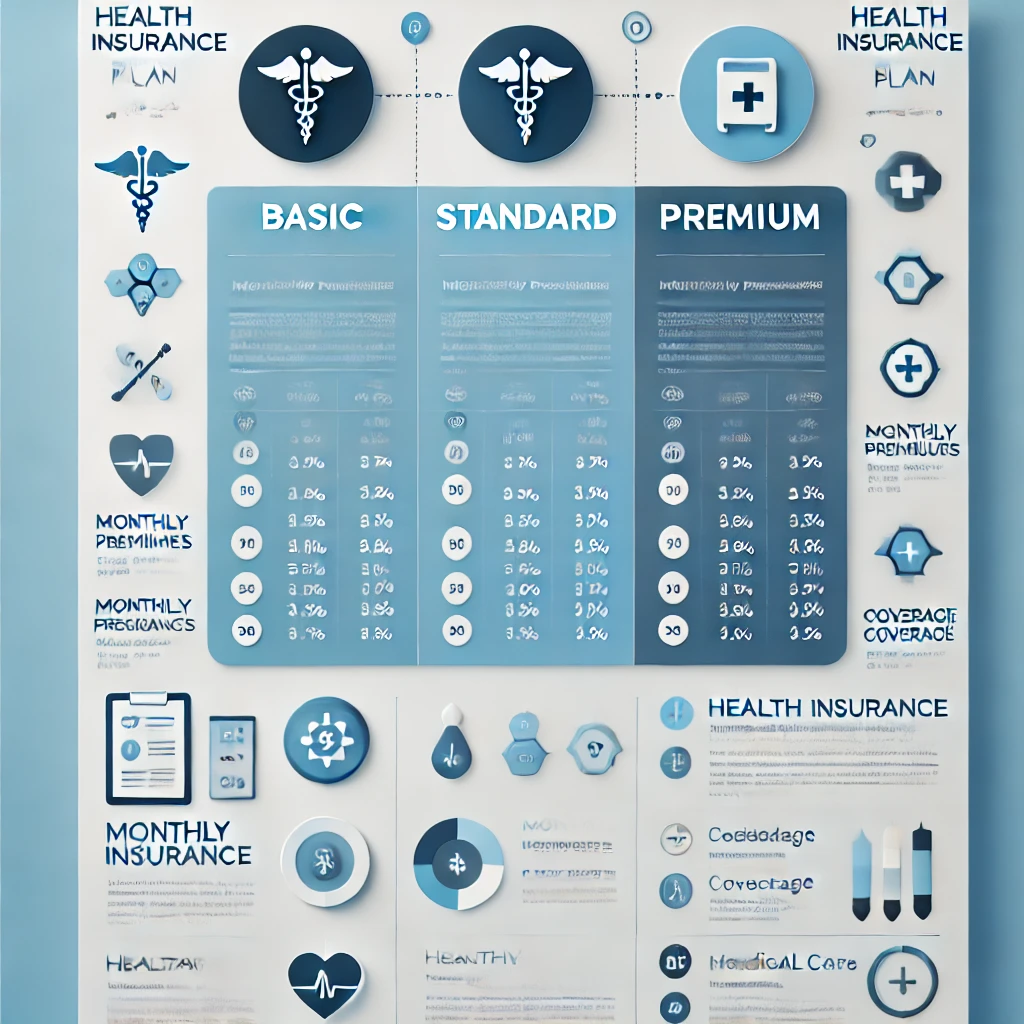

Health Insurance Plan Comparison

| Plan Name | Premium | Deductible | Coverage |

|---|---|---|---|

| Basic Health Plan | $200/month | $1,500 | 80% |

| Standard Health Plan | $300/month | $1,000 | 90% |

| Premium Health Plan | $400/month | $500 | 100% |

Selecting the right health insurance plan for your family is one of the most critical financial and healthcare decisions you will make. With so many options available, it can feel overwhelming to navigate the process. The right plan should provide adequate coverage while being affordable and meeting your family’s specific healthcare needs. Here’s a detailed guide on how to choose the best health insurance plan for your family.

1. Assess Your Family’s Healthcare Needs

Before choosing a health insurance plan, evaluate your family’s medical needs and history. Consider the following factors:

- How often do you and your family members visit the doctor?

- Do any family members have chronic illnesses that require ongoing treatment?

- Are there upcoming medical procedures, pregnancies, or specialist consultations needed?

- Do you frequently need prescription medications?

- Do you prefer specific doctors or hospitals?

Understanding your family’s medical requirements will help you determine what type of coverage and benefits are essential in a health insurance plan.

2. Understand Different Types of Health Insurance Plans

Health insurance plans come in various types, each with different levels of coverage, flexibility, and costs. The most common types include:

a) Health Maintenance Organization (HMO)

- Requires you to select a primary care physician (PCP)

- Requires referrals for specialists

- Generally lower premiums and out-of-pocket costs

- Limited to in-network providers

b) Preferred Provider Organization (PPO)

- Offers flexibility to see specialists without referrals

- Allows both in-network and out-of-network coverage (higher costs for out-of-network)

- Higher premiums compared to HMO plans

c) Exclusive Provider Organization (EPO)

- Similar to an HMO but does not require referrals for specialists

- No out-of-network coverage except in emergencies

- Lower premiums than PPO plans

d) Point of Service (POS)

- Requires a primary care physician

- Allows out-of-network coverage at higher costs

- Offers some flexibility for specialist visits

Each of these plans has advantages and disadvantages, so it’s important to consider what suits your family’s needs best.

3. Compare Costs: Premiums, Deductibles, Copayments, and Out-of-Pocket Maximums

Health insurance costs include several components:

- Premiums: The monthly amount you pay for insurance coverage.

- Deductible: The amount you must pay out-of-pocket before your insurance starts covering expenses.

- Copayments and Coinsurance: Your share of costs for doctor visits, prescriptions, and other services.

- Out-of-pocket maximum: The maximum amount you will pay annually before your insurance covers 100% of expenses.

Finding the right balance between premiums and out-of-pocket expenses is crucial. If your family frequently visits doctors or needs regular medications, a plan with a lower deductible and higher premium might be more cost-effective. Conversely, if you are relatively healthy and don’t need many medical services, a high-deductible plan with lower premiums may be more affordable.

4. Check the Network of Doctors and Hospitals

Each health insurance plan has a network of doctors, specialists, and hospitals. If you have preferred doctors or hospitals, ensure they are in the plan’s network to avoid high out-of-pocket costs. Out-of-network services can be significantly more expensive or may not be covered at all.

5. Review the Prescription Drug Coverage

If your family members take medications regularly, check the plan’s drug formulary (list of covered medications). Some plans have higher copayments for certain drugs, while others may not cover them at all. Look for plans that offer affordable prescription coverage for the medications you need.

6. Consider Additional Benefits

Some health insurance plans offer additional benefits such as:

- Telemedicine services

- Wellness programs

- Mental health and behavioral therapy coverage

- Vision and dental insurance

- Maternity and newborn care

If any of these benefits are important to your family, ensure they are included in your chosen plan.

7. Look for Family-Friendly Features

When selecting a plan for your family, consider features such as:

- Family deductible limits: Some plans have a combined deductible for the entire family rather than individual deductibles for each member.

- Coverage for children: Ensure routine check-ups, vaccinations, and pediatric care are included.

- Maternity coverage: If you plan to have children, check if prenatal and maternity care is well-covered.

8. Compare Plans Using the Health Insurance Marketplace

In the U.S., you can compare different plans on the Health Insurance Marketplace (Healthcare.gov) or your state’s exchange. If your employer offers health insurance, review the available options carefully. Many employers subsidize a portion of the cost, making employer-sponsored plans more affordable.

9. Understand the Terms and Conditions

Before finalizing a plan, read the terms and conditions carefully. Pay close attention to exclusions, coverage limits, waiting periods, and pre-existing condition clauses. Knowing these details will help prevent unexpected expenses later on.

10. Seek Professional Assistance

If you’re unsure about which plan to choose, consider consulting an insurance broker or healthcare navigator. These professionals can help explain complex terms, compare plans, and identify the best option for your family’s needs.

Conclusion

Choosing the right health insurance plan for your family requires careful consideration of costs, coverage options, and specific healthcare needs. By assessing your family’s medical history, comparing plan types, evaluating costs, and checking provider networks, you can make an informed decision that provides the best possible coverage for your loved ones. Take the time to research and select a plan that offers peace of mind and financial security for the years ahead.